By Jan Faure

Global equity markets posted solid gains in August, buoyed by strong US corporate earnings, improving risk sentiment, and growing expectations that the US Federal Reserve (Fed) will cut interest rates in September. While trade and fiscal uncertainties remain, investors were encouraged by signs of resilience in global activity and a shift in the Fed’s tone to a more accommodating stance.

The primary market mover was July’s US non-farm payrolls report, which revealed a slowing labour market. Significant downward revisions to previous employment figures suggest a more fragile consumer base, raising concerns about the broader economic impact of President Trump’s ongoing trade war.

At the Jackson Hole symposium, Fed Chair Jerome Powell acknowledged a shift in the balance of risks, suggesting that the Fed may need to adjust its policy stance in response to labour market weakness. Powell’s comments reinforced expectations for a rate cut, with investors pricing in a high probability of a 25bps cut at the Fed’s September meeting.

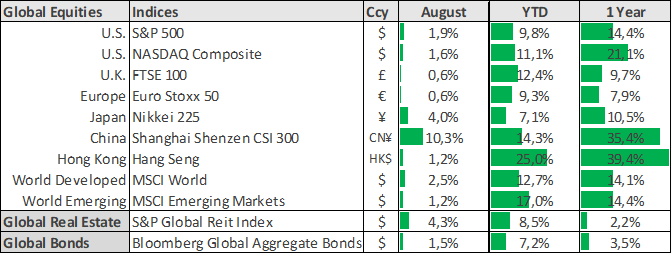

The S&P 500 rose 1.9% for the month, while the Nasdaq Composite gained 1.6%, marking its fifth consecutive positive month. Optimism around the AI trade continued to drive tech stocks higher, with Nvidia’s earnings beat reinforcing investor confidence in the sector.

In Europe, the Euro Stoxx 50 added 0.6%, though gains were capped by political uncertainty. The upcoming 8 September no-confidence vote in France over public spending cuts has rattled European markets, while broader concerns over trade policy and geopolitical tensions remain. ECB President Christine Lagarde signalled caution, noting that eurozone growth may slow this quarter, and that rate decisions will hinge on September’s macroeconomic projections.

Asian markets were broadly positive. China’s CSI 300 index surged 10.3%, driven by government support for domestic chip production and hopes for further stimulus. China’s economy, however, remains constrained by weak consumer sentiment caused by persistent weakness in the housing market. Hong Kong’s Hang Seng Index rose 1.2%, while Japan’s Nikkei 225 gained 4.0%, supported by a new US-Japan trade deal and upbeat economic data.

Meanwhile, President Trump extended the US-China tariff truce for another 90 days, pushing the deadline to November 10. The move is expected to pave the way for a potential meeting with President Xi Jinping in late October. While the extension eases short-term concerns, aligning long-term interests between the two nations remains a formidable challenge.

Looking Ahead

August’s gains reflect a market increasingly confident in central bank support, but risks remain. Elevated valuations, particularly in the US, suggest that much of the good news is priced in. Trade and fiscal uncertainty continue to loom large, and the potential for renewed inflationary pressures cannot be ignored. In this environment, balancing exposure to growth sectors with defensive assets that can weather potential volatility stemming from policy shifts and macroeconomic surprises remains key.

Global Indicators – Local reporting currencies