By Jan Faure

Global markets experienced a volatile February, shaped by shifting interest-rate expectations, geopolitical tensions, and renewed strength in commodity prices. A key theme during the month was the continued broadening of market leadership beyond US mega-cap technology. While technology shares remained influential, value-oriented sectors such as energy, mining, and industrials contributed meaningfully to performance, particularly in commodity-linked markets.

United States

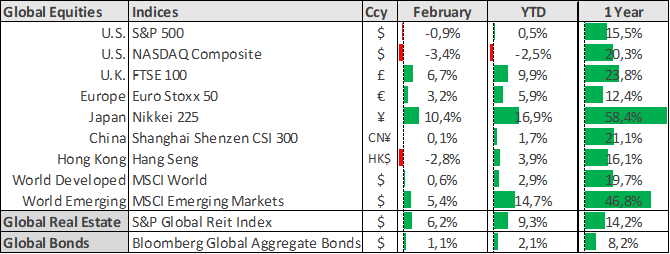

US equity markets experienced notable volatility as investors reassessed interest rate expectations and technology sector valuations. The S&P 500 declined 0.9% for the month, while the Nasdaq Composite fell 3.4% amid continued pressure on technology stocks. In contrast, the more value-oriented Dow Jones Industrial Average gained 0.2%. The divergence between indices reflects an ongoing rotation away from highly valued growth stocks toward more cyclical and defensive sectors.

The major US hyperscaler companies signalled plans to lift AI-related capital expenditure to over US$600 billion in 2026. Although demand for AI-driven services continues to grow strongly, investors have become more focused on the economic returns these massive investments may ultimately generate. As a result, markets are increasingly distinguishing between companies that can translate AI investment into consistent earnings growth and those whose spending is rising faster than their profitability outlook.

Macroeconomic data presented a mixed picture. January inflation moderated to 2.4% year-on-year, down from December’s 2.7%, while core inflation remained sticky at 2.5%. US fourth-quarter GDP growth slowed to 1.4% annualised, below consensus expectations and sharply lower than the 4.4% expansion recorded in the previous quarter. Minutes from the Fed’s latest meeting highlighted differing views among policymakers regarding the appropriate path for interest rates, suggesting a cautious and data-dependent policy approach.

Europe & UK

The Euro Stoxx 50 gained 3.2% for the month, supported by solid corporate earnings and signs that inflationary pressures in the region continue to ease gradually. The FTSE 100 surged 6.7%, reaching record highs as investors rotated toward value-oriented sectors such as energy, mining, and financials. Investors continued to rotate away from mega-cap US technology companies, benefiting both developed and emerging markets outside of the US.

Investors also monitored the policy outlook from the European Central Bank and the Bank of England. Both institutions continued to signal a cautious stance, balancing moderating inflation with the need to maintain financial stability amid persistent geopolitical risks.

Asia

Asian markets delivered mixed performance in February. Japan’s Nikkei 225 continued to benefit from a weaker yen and ongoing corporate reforms aimed at improving shareholder returns. The Nikkei 225 surged 10.4% in February, reaching fresh highs during the month. Expectations for additional fiscal stimulus and supportive monetary policy also helped sustain investor interest in Japanese equities.

Chinese markets remained more subdued as investors weighed ongoing structural challenges in the domestic economy against incremental policy support from authorities. While stimulus measures have provided some support to sentiment, concerns around property markets and slower domestic demand continue to influence investor positioning. The CSI 300 Index rose 0.1% for the month while Hong Kong’s Hang Seng Index declined -2.8%.

Commodities

Commodities were among the strongest performers during February. Precious metals continued to attract investor demand as geopolitical risks and currency volatility supported safe-haven buying. Gold remained close to record highs during the month, reflecting persistent demand from both institutional investors and central banks.

Industrial commodities also strengthened, supported by expectations of improving global growth and renewed demand from emerging markets. The rally in resource prices provided a significant tailwind for commodity-exporting economies and equity markets with large exposure to mining and energy companies.

Escalating tensions between the United States and Iran raised concerns about potential disruptions to energy supply routes through the Strait of Hormuz, pushing Brent crude oil prices up 2.5% during the month (+19.1% YTD).

Looking Ahead

Market dynamics are shifting as equity leadership broadens beyond the narrow group of US mega-cap technology companies that dominated global returns in recent years. Market breadth has strengthened significantly, with value-oriented and cyclical sectors benefiting from improving global activity and higher commodity prices.

While inflation appears to be moderating gradually, central banks are likely to maintain a cautious approach to policy easing especially given recent events in the Middle East. The armed conflict between the US and Iran, if prolonged, is likely to impact the trajectory of inflation and the durability of global economic growth.

Against this backdrop of geopolitical risks and policy uncertainty, volatility is likely to remain a feature of the investment landscape. Diversification across regions, sectors and asset classes therefore remains essential. A balanced allocation to equities, real assets and high-quality fixed income can help investors navigate an environment where opportunities remain present, but risks continue to evolve.

Global Indicators – Local reporting currencies