By Jan Faure

Global equity markets extended their rebound in June, buoyed by easing geopolitical tensions, progress in trade negotiations, and surprisingly benign inflation data. Risk appetite returned as investors looked past early-month volatility driven by the Israel-Iran conflict and focused instead on corporate developments and potential rate cuts from the US Federal Reserve.

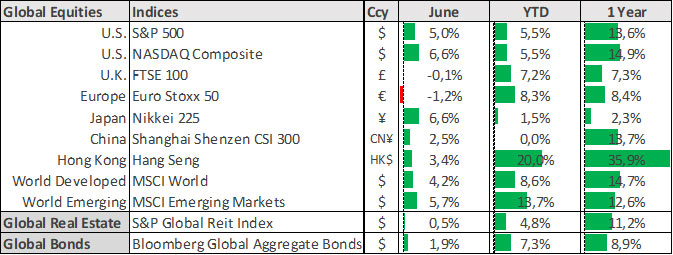

US equities closed out the first half of 2025 on a high, with the S&P 500 and Nasdaq reaching fresh all-time highs. The S&P 500 climbed 5.0% (+5.5% YTD) while the Nasdaq surged 6.6% for the month (+5.5% YTD). Gains were driven by ‘big tech’, easing trade tensions, and growing expectations for Fed rate cuts later this year.

The geopolitical backdrop remained tense. The Israel-Iran conflict escalated mid-month, with US airstrikes targeting Iranian nuclear facilities. Oil prices spiked as markets feared supply disruptions, pushing Brent crude above $80/bbl. However, a US-brokered ceasefire on 24 June helped ease tensions, with Brent settling near $68/bbl by month-end. While the ceasefire remains fragile, markets responded positively, and risk sentiment improved.

In economic data, US May CPI inflation rose 2.4% YoY (vs. 2.3% in April), encouragingly below the 2.5% consensus. Core CPI held steady at 2.8%, also undershooting expectations. The Fed’s preferred inflation gauge, core PCE, ticked up to 2.7% YoY from a revised 2.6%. The softer inflation backdrop, combined with signs of economic softness, has fuelled market hopes for a rate cut in the second half of the year.

At its 18 June meeting, the Federal Reserve held rates steady at 4.25–4.50% but cut its 2025 growth forecast to 1.4% and raised its inflation outlook to 3.0%. Unemployment is now expected to rise to 4.5% from 4.2%. Fed Chair Jerome Powell acknowledged that tariffs are likely to push prices higher but reiterated that the Fed remains in a wait-and-see mode. He noted that the full impact of tariffs is still unfolding and that the Fed may soon face a challenging trade-off between rising inflation and slowing growth. While Powell emphasized that the job market does not urgently require a rate cut, markets latched onto dovish signals from other FOMC members, who suggested that cuts could be appropriate if inflation remains contained.

European and UK markets edged lower amid mixed inflation data and policy uncertainty. The Euro Stoxx 50 index declined 1.2% for the month (+8.3% YTD) while the UK’s FTSE 100 was flat (+7.2% YTD). Eurozone headline inflation eased to 1.9% YoY, dipping below the ECB’s 2.0% target for the first time since 2024.

In Asia, performance was mixed. Hong Kong’s Hang Seng rose 3.4% (+20.0% YTD), supported by a tech-led rally and optimism around Chinese stimulus. China’s CSI 300 gained 2.5% (flat YTD) as Beijing’s monetary and fiscal support measures helped offset weak export demand. Japan’s Nikkei 225 jumped 6.6% for the month (+1.5% YTD) despite concerns over trade risks and rising inflation.

Looking ahead, investor focus will shift to the upcoming US jobs report and Q2 earnings season, which may offer further insight into the economic impact of tariffs. While the ceasefire in the Middle East and softer inflation data have boosted risk sentiment, rising US fiscal deficits and looming tariff deadlines remain key headwinds. Markets are cautiously optimistic, but volatility is likely to persist as the Fed navigates a complex policy landscape.

Table 1: Global Indicators – Local reporting currencies