By Jan Faure

Global markets opened 2026 on a volatile footing as politics and geopolitics drove sharp intra‑month swings. Even so, most major equity indices finished higher in January. Global stocks advanced with returns broadening beyond US mega‑caps as a weaker US dollar and resilient data supported risk appetite. Commodities rallied sharply before retracing late in the month.

Markets were rocked by headline risk tied to the US administration’s increasingly confrontational stance on trade and foreign policy, most notably the Greenland‑linked tariff threats on European allies and a subsequent Davos reversal, which sparked both sell‑offs and relief rallies. Separately, the White House nominated Kevin Warsh to succeed Jerome Powell as Federal Reserve chairman, a move investors interpreted as a signal of continuity and policy discipline, which contributed to a late‑month reversal in safe‑haven positioning.

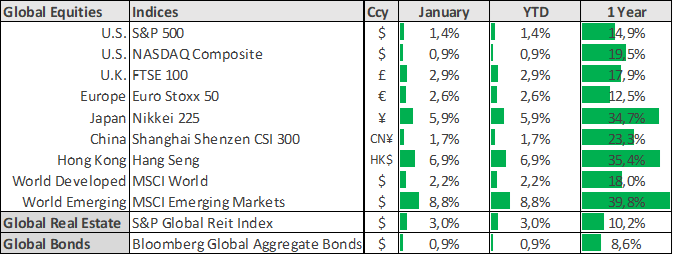

The S&P 500 gained 1.4% in January while the Nasdaq Composite added 0.9%. Fourth quarter company earnings were in focus. Investors focused attention on whether large AI-related capex translates into visible monetization, with results from key platform and hardware names shaping the narrative. Equity returns continued to broaden outside the US technology sector, with most markets outperforming the S&P 500.

Macro data offered a constructive backdrop. December US headline inflation (CPI) printed 2.7% year-on-year (and core inflation 2.6%), the softest readings of the cycle, reinforcing the view that inflation continues to cool. The data reduces the probability of near-term policy tightening, supporting equities.

At its January 28 meeting, the Fed held rates at 3.50%–3.75%. Chair Powell said the downside risks to employment and upside risks to inflation have both diminished. Fed officials said inflation is expected to ease but remains too high to justify rapid policy easing. With macroeconomic data mostly surprising to the upside, it pushes back against aggressive rate-cut expectations.

In Europe, the Euro Stoxx 50 gained 2.6% for the month despite tariff‑related volatility, supported by resilient macro data and earnings momentum. In the UK, the FTSE 100 breached the 10,000 level for the first time and finished the month 2.9% higher, aided by value sectors (energy, miners, defence).

Japan’s Nikkei 225 advanced 5.9% for the month, helped by yen weakness and expectations for additional fiscal support. Hong Kong’s Hang Seng rallied 6.9% while China’s CSI 300 posted more modest gains (+1.7%) as investors weighed a record 2025 trade surplus against subdued domestic demand.

Gold and silver, along with numerous other commodities, spiked to fresh records intra‑month as investors sought safety amid geopolitical tension and dollar weakness, before falling sharply in the final session after the Warsh nomination was perceived as a dollar‑supportive development.

Looking Ahead

We continue to see scope for equity market returns to extend beyond US large‑cap technology as earnings growth becomes more evenly distributed across regions, sectors, and factors. Europe, Japan and selected EMs outperformed in January, and we expect that diversification will remain rewarded if liquidity and growth stay supportive.

Against a still‑benign inflation backdrop and a patient Fed, our emphasis remains on quality and resilience: balance‑sheet strength, sustainable margins, and cash‑flow visibility. Given ongoing geopolitical tail risks, a measured allocation to real assets and alternatives can improve portfolio robustness, while fixed income can continue to function as a ballast on spikes in risk aversion.

A volatile start to 2026 nonetheless delivered positive equity returns, a reminder that improving macro trends can offset policy turbulence. We expect more balanced earnings leadership and episodic volatility as markets digest Fed transition headlines and geopolitics. Staying diversified across regions and factors, with a tilt to quality and select hedges (real‑assets and other alternatives), remains in our view the pragmatic way to compound through the noise.

Global Indicators – Local reporting currencies