By Jan Faure

Globalequity markets endured a volatile November as investor concerns about overextendedvaluations of AI-linked technology companies weighed on sentiment. US equitieswere particularly turbulent, with early-month losses driven by profit-taking intechnology sectors and mounting scepticism about the sustainability ofAI-driven growth. However, the combination of weaker economic data and risingconfidence in policy easing supported markets in the final week of Novemberhelping erase earlier losses.

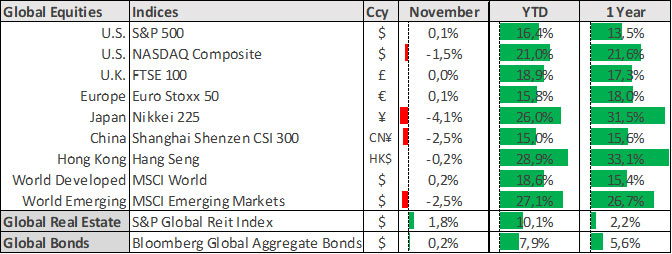

United States

US equitiesdelivered a mixed performance in November. The Nasdaq Composite fell 1.5%,snapping a seven-month winning streak, as investors reassessed loftyexpectations for AI profitability. Despite stellar quarterly results fromNVIDIA, concerns lingered over whether ambitious growth targets across the AIecosystem can be met. The S&P 500 eked out marginal gains, supported by arotation into defensive sectors such as healthcare and consumer staples.

Policyexpectations dominated headlines. A growing conviction that the Federal Reservewill adopt a dovish stance in December helped lift sentiment late in the month.Multiple Fed officials signalled openness to rate cuts amid a weakening labourmarket, even as inflation remains elevated. Markets now price a 90% probabilityof a December rate cut, reflecting both economic softness and politicalpressure from the Trump administration for faster easing.

Politicaldevelopments added complexity. President Trump signed legislation ending thelongest US government shutdown in history after a contentious Senate vote.While the deal funds most agencies until January 30, unresolved disputes overthe Affordable Care Act risk another shutdown early next year. The prolongedclosure cost an estimated $7–14 billion in lost productivity (1.5% of Q4 GDP)and created permanent gaps in economic data, complicating the Fed’sdecision-making process.

Europe

Europeanmarkets were muted in November. The Euro Stoxx 50 gained just 0.1%, while theFTSE 100 ended flat, as investors weighed mixed macro signals against abackdrop of cautious central bank policy. While Eurozone inflation remainsslightly above target, recent GDP figures suggest resilience, limitingnear-term pressure for policy shifts by the European Central Bank.

Asia

Asian equitiesretreated after strong year-to-date gains. China’s CSI 300 fell 2.5%, as weakdomestic demand and slowing momentum in key indicators continued to weigh onsentiment. Japan’s Nikkei 225 dropped 4.1%, reflecting profit-taking after astellar October rally. Broader Asian markets faced headwinds from moderatingglobal growth expectations and uncertainty around AI capital efficiency.

Commodities

Preciousmetals extended their rally. Silver surged to a record high, up over 90%year-to-date, driven by supply constraints and robust industrial demand.Inventories on the Shanghai Futures Exchange fell to near-decade lows, whileETF inflows accelerated, signalling institutional positioning for a sustainedrally. Gold rose 6%, marking a fourth consecutive monthly gain, supported bysafe-haven demand and central bank buying.

Looking Ahead

Markets enterDecember with optimism that the Federal Reserve will deliver a rate cut,reinforcing expectations for easier monetary conditions. However, geopoliticalrisks and lingering political uncertainty continue to cast a shadow over theoutlook. Elevated valuations, particularly in the technology sector, andfragile economic data suggest that volatility is likely to persist, makingdiversification and a focus on quality essential.

Global Indicators – Local reporting currencies