By Jan Faure

Global equity markets posted modest gains in July, supported by strong US corporate earnings, improving risk sentiment, and easing trade tensions. While investor optimism lifted markets early in the month, momentum faded toward month-end as concerns over policy uncertainty and stretched valuations resurfaced.

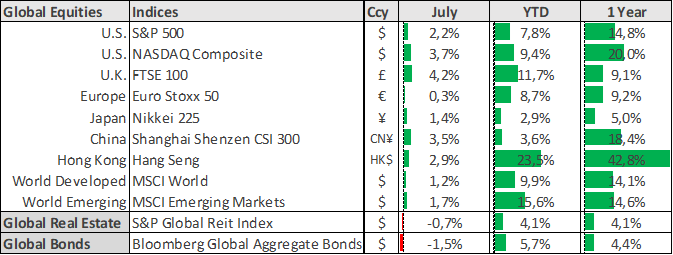

The S&P 500 rose 2.2%, led by semiconductor and AI-related stocks, while the Nasdaq Composite surged 3.7%, extending its winning streak on the back of robust earnings and easing trade tensions. In Europe, the FTSE 100 gained 4.2%, outperforming the Euro Stoxx 50, which edged up 0.3% amid mixed economic data and geopolitical risks. Asian markets were broadly higher, with China’s CSI 300 up 3.5% and Hong Kong’s Hang Seng rising 2.9%, buoyed by stimulus optimism and infrastructure spending. Japan’s Nikkei 225 added 1.4%.

Trade negotiations dominated headlines. The US reached agreements with the EU and Japan, imposing 15% tariffs on most exports while securing investment commitments. Japan pledged $550 billion in US-bound investments, primarily in strategic sectors. Meanwhile, new levies were introduced on Brazil (50%), India (25%), and Canada (35%), although USMCA-covered goods remain exempt. Despite the elevated tariff regime, well above the pre-Trump average of 2.4%, markets welcomed the reduced risk of escalation.

The Federal Reserve held rates at 4.25%–4.50%, maintaining a cautious stance amid persistent inflation and trade-related uncertainty. While Q2 GDP surprised to the upside at 3.0% annualised, the figure was inflated by a collapse in imports rather than domestic strength. The Fed reiterated its data-dependent approach, with Chair Jerome Powell facing political pressure to cut rates. President Trump’s preference for a 1% policy rate has sparked concerns over Fed independence, though Powell is expected to serve out his term through to May 2026.

In Europe, the ECB kept rates unchanged for the first time in over a year, as headline inflation (CPI) hit 2.0% and trade negotiations clouded the outlook. Eurozone GDP rose 0.1% in Q2, narrowly beating expectations, with strength in Spain and France offsetting weakness in Germany and Italy.

Second-quarter company earnings provided a strong tailwind. Nearly 80% of S&P 500 companies beat consensus estimates, with Microsoft, Meta, and Alphabet delivering standout results. The monetization of AI-related capital investments was a key theme, reinforcing investor confidence in the sector’s long-term growth potential.

Geopolitical tensions continued to simmer but remained contained. The fragile ceasefire between Israel and Iran held throughout July, helping stabilize oil markets. Brent crude ended the month at $72.5/bbl, a gain of 7.3%. Gold prices were flat for the month, hanging onto strong year-to-date gains of 27%, and supported by central bank buying and lingering macro uncertainty.

The extended equity market rally since early-April has stretched valuations. Recent US economic data has shown evidence of a weakening US jobs market, raising hopes for interest rate reductions by the Federal Reserve. Markets have been cautiously optimistic, but volatility is likely to persist as the future path of inflation and economic growth in the US remains uncertain. Diversification remains essential.

Global Indicators – Local reporting currencies