Market Review - April 2026

Market Review - April 2026

By Jan Faure

Energy shock dominates as war with Iran redraws the macro outlook

Global markets endured a difficult March as the US-Israeli war with Iran moved from a geopolitical risk into this year’s defining macroeconomic event. Iran’s disruption of traffic through the Strait of Hormuz transformed the conflict into a global energy shock, sending crude oil sharply higher and forcing investors to reprice inflation, growth and policy expectations. The result was a broad risk-off move across asset classes: equities sold off, bond markets weakened as yields rose, and investors shifted away from the view that central banks would be able to ease monetary policy in the near term.

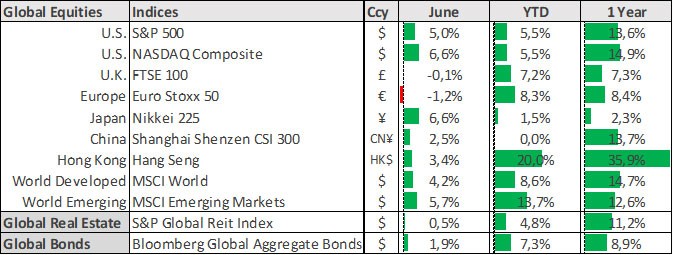

Developed market equities (MSCI World) declined 6.6% for the month while emerging markets (MSCI EM) tumbled 13.3%. Global bonds (-3.1%) fell on inflation and rate hike fears while the US dollar rallied against most major currencies. Gold, which is often seen as a hedge against geopolitical risk, declined by 12% as the policy-rate outlook outweighed gold’s safe-haven appeal.

With the Strait of Hormuz remaining obstructed, markets were forced to confront the possibility that this would not be a short-lived geopolitical spike, but a more persistent supply shock. Brent crude moved above US$110 per barrel, while the International Energy Agency responded with the largest coordinated emergency stock release in its history, making 400 million barrels available to the market. That intervention helped cushion the blow, but did not eliminate it. The deeper concern for investors was that higher energy and shipping costs would feed directly into inflation, eroding real incomes and complicating the outlook for both consumers and policymakers.

That shift was reflected clearly in central bank expectations. At its 17–18 March meeting, the Federal Reserve left rates unchanged at 3.50%–3.75% and explicitly noted that developments in the Middle East had increased uncertainty around the outlook. Fed chair Jerome Powell’s message was not one of reassurance so much as restraint: the Fed can afford to wait, but it cannot assume the inflation impact of the war will quickly fade. In practical terms, March marked a meaningful reversal in the market’s easing narrative. The conversation moved away from when the next rate cut will be towards how long policy may need to remain restrictive if the energy shock proves persistent.

The international implications are also becoming clearer. Asia sits at the centre of the vulnerability story because many of the region’s economies remain heavily reliant on energy flows linked to Hormuz. The conflict’s impact extends beyond crude prices into LNG, petrochemicals, freight costs and broader supply chains.

Late in the month, some of the pressure eased as reports suggested Washington may be more focused on ending the campaign than on securing an immediate full reopening of Hormuz. That prompted a relief move in oil and a rebound in risk assets. Even so, the broader takeaway from March is that markets are now treating the conflict as a macro event, not just a geopolitical one. Until there is greater confidence that energy flows can normalise on a sustained basis, investors are likely to remain sensitive to every development affecting oil supply, inflation expectations and the policy path.

Looking Ahead

The operational status of the Strait of Hormuz remains the critical variable for markets. If disruption persists, the most likely consequence is a more difficult combination of slower growth, firmer inflation and delayed policy easing - a mix that tends to challenge both equities and duration simultaneously. That keeps the case for diversification intact. Quality equities, selective real assets and resilient balance sheets remain important in an environment where geopolitical developments are now driving the macro narrative. March was a reminder that when energy becomes the constraint, markets quickly move from pricing optimism to pricing fragility.

Table 1: Global Indicators – Local reporting currencies